ESG Landscape for United States and Europe

2025-02-07

As Environmental, Social, and Governance (ESG) considerations continue to shape corporate strategies, understanding ESG regulations is crucial for businesses worldwide. This blog explores the evolution of ESG, key frameworks, and current regulatory landscapes in the United States and Europe.

The Evolution of ESG

The concept of ESG has evolved over several decades, transitioning from corporate social responsibility (CSR) to a structured framework for sustainable business practices. Some key milestones in ESG evolution include:

- 1973 – Interfaith Centre on Corporate Responsibility (ICCR) was founded, marking early shareholder advocacy for responsible investing.

- 1985 – Detection of the ozone hole triggered increased corporate responsibility efforts.

- 2000 – Carbon Disclosure Project (CDP) and Global Reporting Initiative (GRI) were established, laying the foundation for modern ESG reporting.

- 2015 – Adoption of the Paris Agreement and the Task Force on Climate-related Financial Disclosures (TCFD), reinforcing climate action commitments.

- 2024 – The Corporate Sustainability Reporting Directive (CSRD) becomes a mainstream requirement in Europe.

This journey highlights how ESG has shifted from voluntary efforts to mandatory regulatory compliance.

Key ESG Frameworks

ESG reporting and compliance are guided by multiple frameworks, categorized as reporting frameworks, benchmarks, and target-setting frameworks.

1. Reporting Frameworks

These frameworks provide guidance on how companies should disclose their ESG data:

- GRI (Global Reporting Initiative): Most widely used, covering various ESG topics across industries.

- TCFD (Task Force on Climate-related Financial Disclosures): Focuses on climate-related financial risks and governance.

- CSRD (Corporate Sustainability Reporting Directive): Mandatory for EU companies, requiring detailed sustainability disclosures.

2. Benchmarking & Scoring Systems

These allow investors and stakeholders to compare companies' ESG performance:

- DJSI (Dow Jones Sustainability Index): Ranks companies based on ESG performance.

- GRESB: Scores ESG performance of real estate and infrastructure investments.

3. Target-Setting Frameworks

These help companies establish sustainability goals:

- CDP (Carbon Disclosure Project): Aims to increase transparency in environmental impacts.

- SBTi (Science-Based Targets Initiative): Helps companies set emission reduction targets aligned with climate science.

- SDGs (Sustainable Development Goals): Provides 17 global sustainability goals.

Understanding these frameworks is essential for businesses aiming to align with regulatory requirements and investor expectations.

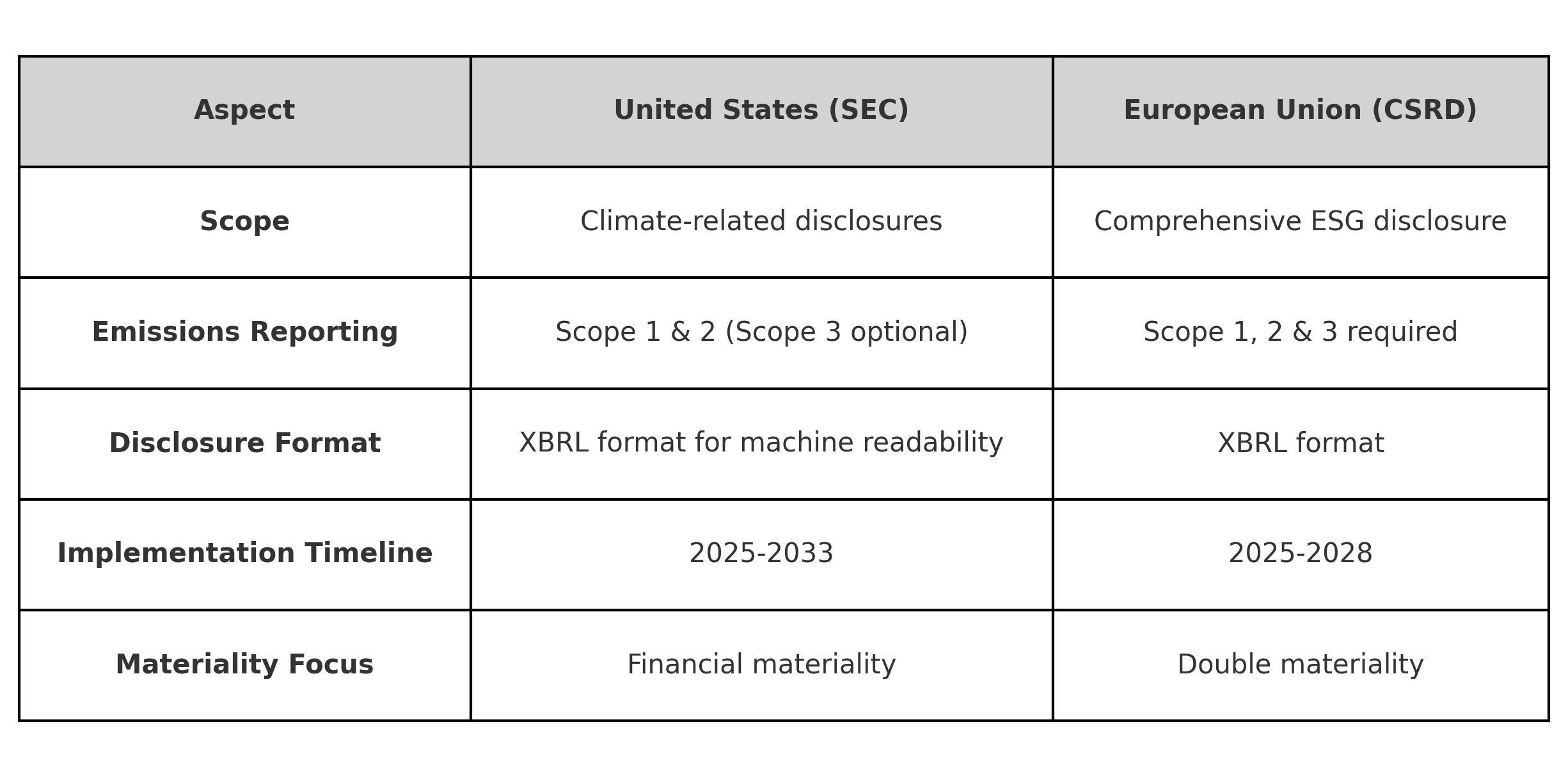

ESG Regulations in the United States

The U.S. Securities and Exchange Commission (SEC) and state-specific laws are driving ESG regulations in the country.

SEC Climate Risk Disclosure Rule

In 2021-2022, the SEC proposed new climate disclosure rules to enhance transparency in corporate sustainability efforts. The rule includes:

- Climate risk disclosure

- Deferred disclosures (scenario analysis, internal carbon pricing, transition plans)

- GHG Emissions Reporting (Scope 1 & 2) (Scope 3 is optional if material)

- Machine-readable reporting (XBRL format)

Implementation Timeline:

- 2025: Large accelerated filers begin climate risk disclosures.

- 2026: GHG emissions disclosures required.

- 2029-2033: Assurance requirements for GHG emissions introduced.

While Scope 3 emissions are not yet mandatory, companies are encouraged to prepare for future requirements.

California ESG Regulations (SB-253 & SB-261)

California has introduced two key regulations impacting companies operating in the state:

- SB-253 (Climate Corporate Data Accountability Act) – Requires disclosure of Scope 1, 2, and 3 GHG emissions starting in 2028.

- SB-261 (GHG Climate-Related Financial Disclosure Act) – Mandates financial disclosures on climate risks from 2027.

These regulations expand beyond federal requirements, pushing companies toward more transparent sustainability reporting.

ESG Regulations in Europe

Europe leads in ESG regulations, with CSRD and EU Taxonomy setting new sustainability disclosure standards.

Corporate Sustainability Reporting Directive (CSRD)

CSRD expands ESG reporting requirements across the EU, replacing the Non-Financial Reporting Directive (NFRD). Key features include:

- Double materiality: Requires companies to disclose both how sustainability impacts their business and how their business impacts the environment and society.

- Mandatory ESG reporting: Financial and non-financial disclosures are required.

- XBRL format: Ensures data is machine-readable for better comparability.

Implementation Timeline:

- 2025: Large EU companies (previously under NFRD) must report for FY 2024.

- 2026: Other large companies begin compliance.

- 2027: Listed SMEs start reporting.

- 2028: Non-EU companies with significant EU operations must comply.

CSRD aligns with GRI, TCFD, and SBTi, ensuring global standardization in sustainability disclosures.

EU Taxonomy for Sustainable Activities

The EU Taxonomy classifies environmentally sustainable economic activities. It is used by investors and businesses to assess ESG alignment.

Key requirements:

- Companies must disclose how much of their revenue and capital expenditure aligns with EU Taxonomy principles.

- Helps prevent greenwashing by establishing clear sustainability criteria.

Comparing U.S. vs. European ESG Regulations

Final Thoughts: Preparing for ESG Compliance

With ESG regulations evolving globally, companies must:

- Understand regulatory requirements in their operating regions.

- Align ESG strategies with frameworks like CSRD, SEC, and SBTi.

- Leverage ESG reporting tools to ensure accurate, machine-readable disclosures.

- Engage investors and stakeholders by showcasing sustainability commitments.

As ESG compliance becomes a business imperative, companies must proactively integrate sustainability into their operations and reporting.