Construction Emissions Uncovered: Turning Hidden Emissions into Net Zero Action

2025-06-27

In the 11th session of the Navigating Net Zero series, we explored one of the most overlooked and challenging emission sources—construction-related GHG emissions. The session offered a practical deep dive into carbon accounting for a real construction project and outlined how these emissions can impact a company’s net-zero strategy.

Case Study: A Commercial Campus Construction in India

We examined the carbon footprint of a large public sector undertaking (PSU) constructing a commercial headquarters campus with: - Total construction area: 78,443 sqm - Three parts: Block A (B+G+M+7F), Block B (B+G+M+12F), and MLCP with staff quarters (7F each) - Dedicated DG shed and services building already constructed

Important Note: Construction was outsourced to a construction company, while the emissions reporting was required for the PSU (the reporting company).

Understanding the Boundaries for GHG Accounting

Organizational Boundary

- Construction Company: Executes the work

- Reporting Company (PSU): Takes operational control post-construction and is responsible for reporting capital goods emissions

Operational Boundary

GHG inventory was limited to the construction phase, excluding operational or post-handover emissions.

Carbon Accounting Approach & Activity Mapping

Carbon emissions = Activity Data × Emission Factor

Activity Data Types

- Fuel consumption (litres/kgs)

- Electricity use (kWh)

- Materials used (kgs, sqm)

- Transportation distances (ton-km)

- Waste generated (kgs)

Emission Factor Sources

- CEA India (electricity)

- UK DEFRA (transport, fuels)

- ICE Database (construction materials)

- India GHG Program, USEPA

Scope-Wise Emission Categorization

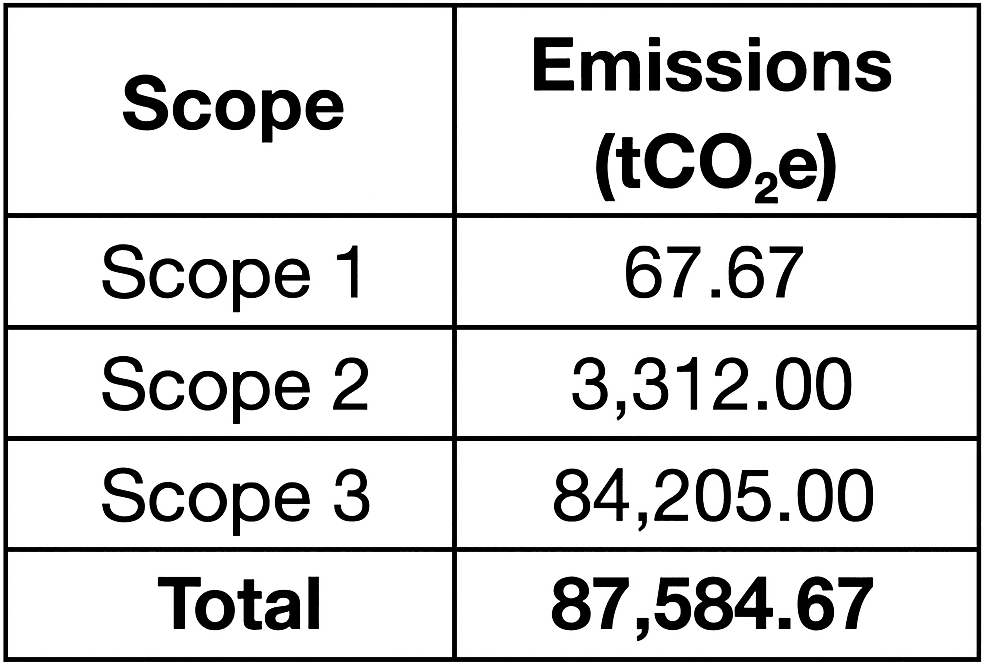

Scope 1 (Direct Emissions)

- DG set diesel use: 15,000 L → 40 tCO₂e

- Construction vehicles: 10,000 L → 27 tCO₂e

Scope 2 (Indirect Electricity Use)

- Grid power for construction: 4 million kWh → 3,312 tCO₂e

Scope 3 (Value Chain Emissions)

Purchase of Goods & Services:

- Cement (15M kg): 12,866 tCO₂e

- Steel, concrete blocks, tiles, admixtures, etc.

Upstream Transportation:

- 69 million ton-km → 6,900 tCO₂e

Employee Commuting:

- Mixed transport: ~1 tCO₂e

Upstream Leased Assets:

- Equipment like cranes/saws: 7,700 tCO₂e

HVAC System:

- 4,500 TR estimated → 6,667 tCO₂e

Electricals & Furniture:

- 3,500 sqm (furniture): 123 tCO₂e

Waste Generated:

- 2,680 tons of waste → 1,954 tCO₂e

Fuel and Energy-Related Activities:

- Well-to-tank emissions and T&D losses

Downstream Transport:

- Waste to landfill → 8.04 tCO₂e

Total Emissions Summary (Construction Company Perspective)

Translating for the Reporting Company (PSU)

For the PSU, all construction emissions are accounted as Scope 3 – Capital Goods.

- Capital Goods Emissions: 87,584 tCO₂e

- Site Visit Travel (mobile combustion): ~30 tCO₂e

This distinction is crucial for ESG reporting under frameworks like BRSR, GRI, and TCFD.

Towards Net Zero: Timeline vs. Life Cycle Views

Annual Net Zero Roadmap

- Considers yearly emissions and offsets

- Possible achievement by 2037 through progressive reductions and offsets

Cumulative Net Zero (Life Cycle View)

- Includes embodied emissions from construction

- Requires higher cumulative offsets (~846,000 tCO₂e)

- Net Zero achieved by 2039 with accelerated offsetting

Conclusion

Construction emissions are no longer invisible. As sustainability moves from intent to action, the ability to measure, manage, and mitigate construction-phase emissions is essential. Whether you’re a builder, consultant, or asset owner, factoring in embodied carbon and creating a robust offset strategy is key to credible net-zero action.

Need help mapping construction emissions? Contact us at [email protected]